# Worked Example

This example walks through a full seven-day epoch with two public models, identical forward returns, and staggered voter deposits.

Symbol

Meaning

Fixed value here

E

Epoch emission

100 SLINKY

τ

Return look-back window

7 days

Ri

Net return over τ

5 % for both models

Ai

Audit pass flag

1 (quorum reached)

## Stake schedule

Model

Voter

Stake (SLINKY)

Day deposited

Days locked

Stake-days

A

V1

10

Monday

7

70

V2

20

Thursday

4

80

B

V1

20

Monday

7

140

V2

30

Wednesday

5

150

ΣA=30, ΣB=50

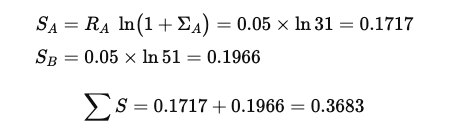

## Slinky Scores

Model shares

## Pool allocation and 50 : 50 split

| Model | Pool share (SLINKY) | Creator 50 % | Curator pool 50 % |

| ----- | ------------------- | ------------ | ----------------- |

| A | 46.62 | 23.31 | 23.31 |

| B | 53.38 | 26.69 | 26.69 |

## Curator distribution (stake-days weighting)

Model

Voter

Payout (SLINKY)

A

V1

23.31 × 0.4667 = 10.88

A

V2

23.31 × 0.5333 = 12.43

B

V1

26.69 × 0.4828 = 12.88

B

V2

26.69 × 0.5172 = 13.81

## Observations

* **Diminishing stake influence**: Logarithmic weighting prevents raw capital from overpowering performance. Model B holds 67 % more stake than Model A but earns only 14 % more creator reward.

* **Early conviction rewarded**: V1 in both models receives the larger share of curator emissions despite equal or lower absolute stake due to longer lock duration.

* **Performance oriented**: If Model A had posted 10 % return while Model B stayed at 5 %, Model A’s score would exceed Model B’s even with less capital.